Creating the first paylater App for BUMN that led to obtaining 60,000 new customers in the first Month

2018 - 2019

Ceria by BRI is the Gov Bank’s first paylater app that was catered for consumptive behaviour customers who enjoys shopping for primary, secondary and tertiary needs. The goal of creating this product is to improve the total revenue of BRI by capturing new customer segment, as well as to compete against non financial service authorised banks in Indonesia by offering safety, security and most importantly trust.

Problem

There are numerous number of digital lending products that are not financially serviced authorize causing a lot fraud impressions amongst the general public causing to easily distrust them. With this disruption, BRI needed new strategy for a digital transformation by creating a safer digital lending product to gain new market segment.

Challenge

How to be Gov bank’s #1 safest and securest paylater product across Indonesia? BRI’s majority of their account holders and customer markets are identified as Ultra-Micro customers compare to other large Indonesian banks whose focus are the consumer based market. In addition, we also have to be innovative with simplified ideas without compromising the regulations and compliance

The MVP that we established as an area of focus are:

A. Easy registration and concise steps for credit applications

B. Steps of Transactions through popular merchants

C. Informative guide to complete installment

Project Role

I had the opportunity to become the first designer and along the way build a team of product designers that focuses on growth, application and transactions stream tribe

Designed the first concept for the moonshot app

Supporting in research, prototyping and design thinking initiatives from collaborating with market, development and design vendors

Becoming design lead for the revamp version, including as facilitator for design thinking workshops, lightning decision jams, usability testing

Users & Audience

The are two types of customers which Ceria aims for since its deployment and product iteration. These personas are:

A. Shopaholic: 28 - 35 years old young mature men and women who are passionate active workers, enjoys splurging their money for self-gratification, life fulfillment and dream chasers.

B. Economize: 28 - 35 years old middle age men and women who prioritize their families more than anything. Unselfished and essentials drive who needs things to survive.

Design Principles

My principles have always been: Customer first, Storytelling, Impactful and Simple. The product needs to be customer first minded catering to their needs. The product needs to connect users through a story they can relate to. The product needs to be impactful for both users and the business. The product needs to be simple enough to use for longetivity.

1.1 FGD in Bandung

Discovery

To understand what the customer requires and needs, we first enter the Discovery phase where we conducted FGD (First Group Discussion) . In our short timeline, we wanted to get an overview of business goals, product definition and study current users behavior when it comes to lending money. Although the disadvantage of conducting FGD would lead to users having the same opinion, but this method is more suitable for the timeline and we are able to obtain the insights efficient and effective.

We conducted FGD for 3 different groups in 3 different provinces which are: Java, Sumatra and Sulawesi. The reason for these 3 different provinces is validate our assumptions on which province is likely to spend more money and which province tends to save more money. During the FGD, we have prepared a rundown for all groups as we wanted to ask their daily habits, product concept, perception about BRI, product brand and key message of the product.

1.2 FGD in Makassar

1.3 FGD in Solo

“ Customers are very calculative when it comes to plan their spendings and having a limited space of activities when shopping for extra items ”

During our FGD, we have learned new interesting knowledge in regards to the concept of digital lending. We’ve learned that customers understood the concept of credit line that was being offered by the product concept. When we showed the product concept, they instantly recognize the lending feature is very similar to which that of a credit card. Although they appreciate the fast application process to obtain the credit limit, they show no interest in this product’s speciality because there are lots of lending products out there that offers more interesting value propositions to which that BRI needs to find a better offering.

Customers are very calculative when it comes to plan their spendings and having a limited space of activities when shopping for extra items. They also expect transparent transactions and loan history in order for them to track their lending better, as well as hoping that they can use the product through different online and offline medium channels. This is because customers would like to use the lending product for purchasing mostly tangible products such as electronic, fashion and home appliances. As such, they rarely use lending services for holiday purposes such as buying a ticket for travels and entertainments.

One of the activities we did was in order to get a better understanding of what customers wanted, we presented a draft prototype and engage users in writing singular words and descriptions of how should the product be presented. We wanted to look for a new product name and brand identity that would portray the product and to do so we require the participants to select a mood board that we prepared to obtain customers perception. Since the product is attached to the BRI mindset, majority of the customers see the product requires to show trust, smart, easy and simple while expressing it in a cool and fun matter through cooler and calmer color tone from blue to purple. Ideally, they feel that the product should embody personalities that are young, smart and wise at the same time. They believe it should cater to those who knows how to have fun, while being smart and careful.

Since this is my first experience in supporting an FGD, I’ve learned that customers shows different way of thinking when expressing their needs and desires. In an FGD, the most important thing that interviewers must do is to always keep in check of other customer’s opinions so that they don’t tend to be followers of others. FGD helps us to gather sample datas in depth and more detail allowing us to understand the customers problems better in a way that we can emphatise with them better.

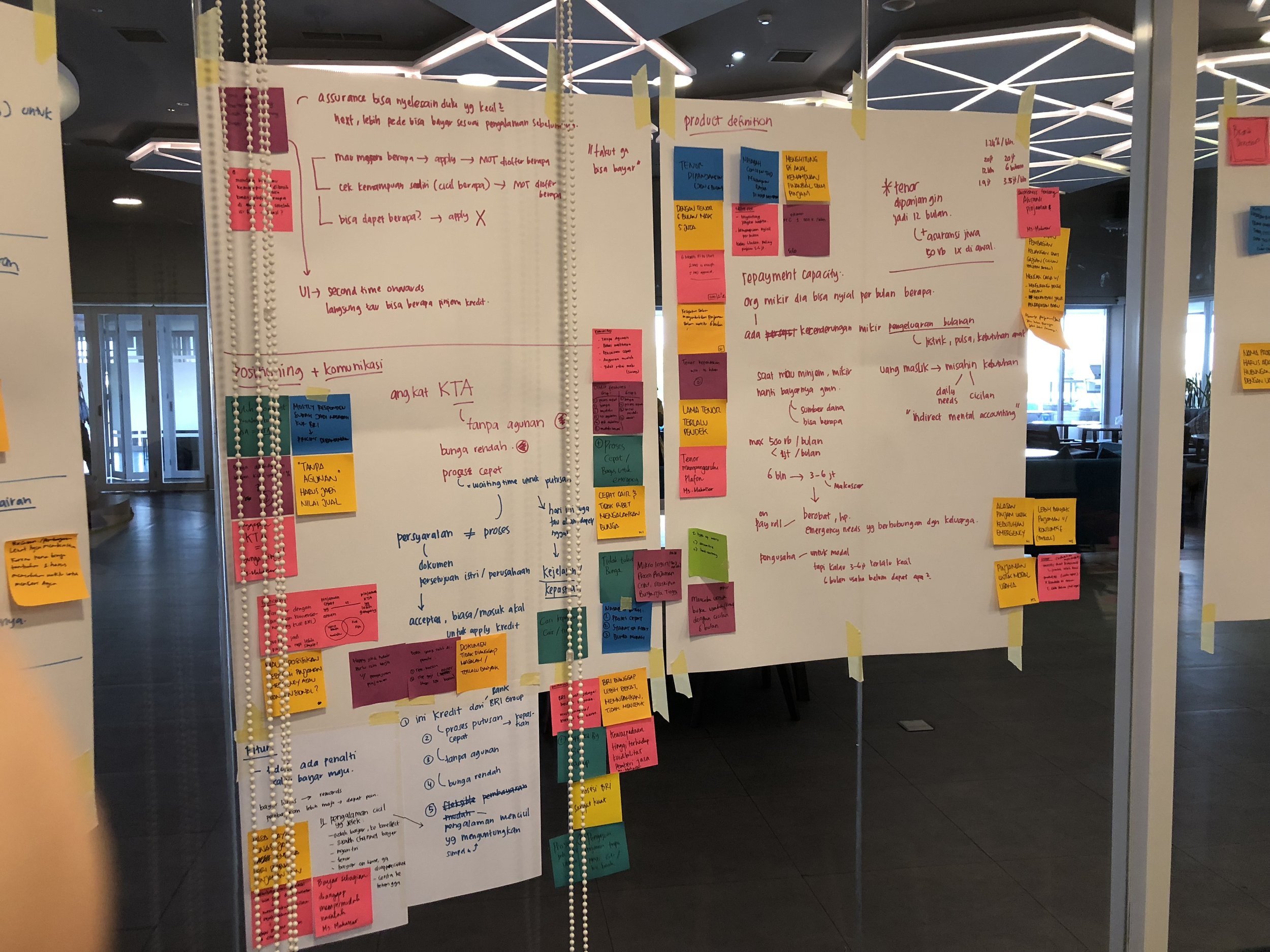

Ideation

The next step of this process is conducting a week of design thinking and lightning decision jam. We require a week to work on this simply because there are lots of grounds to cover. While we are focusing on building the CX blueprint of the product, we need to align all insights from the product owners, business owners, development and design.

The list of activities that we are about to do are:

1. Aligning the problems and needs of customers, as well as business contraints

2. Creating solutions from the problems, narrowing it down to focus areas

3. Analyze draft prototype to improve its user journeys and customer blueprint

4. Decisioning on product naming and brand personality

5. Once 1-4 has been defined, we start to create a next plan of action

During our design thinking sessions, we try to focus on the targeted customers behavior, perception and desire for the product. In this early stage, we looked at how the product would connect to BRI, marketplace and customers without interfering security and compliances of the company. we looked at how the existing business model in BRI when it comes to provide loan as a basis and how might we adapt the concept into a seamless technology environment. We also looked at how competitors and BRI set their interest rate and how might we achieve product differentiation through this aspect. We also analyze as a team on how might existing and new customers would emotionally react when having this product that they can use for their everyday activities.

The biggest challenge in defining the product is that this will be the first digital lending a Gov bank would create and the most disruptive financial technology that BRI would endure since it’s not considered a traditional method of banking. Through this challenge, we hope that not only it gives BRI a new perspective on how lending works through technology, but most importantly how it helps transform the business and bringing more outstanding profits. Overall in this ideation process, our expected outcomes are to identify product business model and customer blueprints, product brand story and technical requirements for BRI. The experience of supporting a design thinking session for the first time is overwhelming because not only I get to focus on the design of the product, but I have to also be able to look at the process from a helicopter view.

“ Although customers understood the initial product concept, it doesn’t stand out or considered even better that other existing solutions out there ”

The additional insights that we gathered from design thinking is that we found out that a 2.14% interest rate is high for every transactions. A lending model should go all the way in digital format as it provides more seamless experience. 1 hour is the best time limit to wait for a credit limit be processed while approving and accessing compliance documents easily. The product should be accessible and use to purchase products in e-commerce platforms such as Tokopedia, Bukalapak, Traveloka and many more while giving the customers full control and trust by providing transparent transaction details every time they make a spending.

Throughout the design thinking process, the main focus is to create better product proposition in order to capitalize the moment and make new opportunities. We came up with several ideas to help make this happened. Firstly, the product should be presented self control instead of self indulgence. It should be aimed to provide a smarter platform so customers won’t go over board when it comes to shop. The key here is to communicate that the product is designed to help customers maintain their spendings and becoming a swiss-army knife for all payment purposes. Secondly, the product can be adjusted into Gov Bank’s first digital hybrid credit card and e-wallet where payments can also come from QR and the first ever Buy Now Pay Later integrated into Gov Bank to expand its product position. Lastly, express and long term loans with different interest rate that is low as possible to suite the market segment of BRI and by engaging them with points and rewards to keep the retention.

By executing the ideas, we can give huge benefits for BRI in not only adding a new portfolio of credit card products and new potential customers, but also a collection of data that can be used to the bank’s credit division advantage that would help them market into untapped customers. It also increase the potential to have loyal customers using the product especially considering that new seamless technology experience is implemented in BRI for the first time.

We moved to the next step and that is naming and identifying the brand identity of the product. Based on the insights that we collected from FGD, customers tended towards on active purple color scheme where it not only represents the youth and energy in a cool/calming matter, but the color itself means wisdom in trust and making decisions. When aligning back to the product proposition, this fits the identification since the aim of the product is to cater the needs of self controlled young customers who enjoys and craves to shop.

We have established three key messages that would describe the brand story of the product:

Opening a pathway to enjoy life: The product is designed to help customers achieve what they want and desire without increasing risk in money management

Helping to shop smartly: Taking advantage on the marketplace as a center of aspiration

Virtual money with a credit card feel: Ease and seamless of payment in various online or offline merchants given an option of installment that brings peace of mind to customers

Our outcome from design thinking are in two parts with specific actionable outcomes:

Feature prioritizations: The four core features and requirements that required to be developed are Onboarding + apply for limit credit, Credit scoring system, Merchant purchasing and Transactional history for installment pay. Development and design are require to collab in timeline delivery and estimation of development to make sure everything is deployed on time.

Product and Brand: Ceria (Cepat Ringan Aman) for consumer needs digital lending with purple brand color that caters for the young and milenial consumptive market. The business and marketing team require to collab in making the right promoting strategy.

Design thinking helps me to understand what matters the most in product development. It is to prioritize which ideas can be manifested into a feature and which ones can be saved in the long run. It is to create solutions to business problems through planned strategy. Ideation through design thinking helps bridge problems from different divisions and discuss altogether on how we can reach the goals together and optimizing the workload better.

The next step validation for product direction as proposed is to identify the demand of traveling services, research in offline transaction features and identifying potential merchants if they are suitable for the digital lending that BRI offers such as H&M, Pull&Bear, Ikea, Ramayana, etc.

Design

Once all ideas and requirements have been agreed by the stakeholders, the next step is designing and prototyping the product itself. My role for this part is to ensure that I get to deliver the necessary business and technical details in the design while being able to be creative without going overboard on the existing business model that BRI is currently maintaining.

Paper Prototype

During the design thinking sessions, everyone participated in a crazy eight activity where everyone starting to sketch different ideas on how the features we all ideate can be translated into a sketch of designs. From all the ideas that everyone explored, we vote on the important key designs and ideas that we believe is important in building the design. We all made paper prototype together before translating it into digital and the reason is with paper we get a sense of real experience and feeling of how customers would respond and react to the product.

Digital Prototype Ver 1

Digital Prototype Ver 2 - Low Fidelity Wireframe

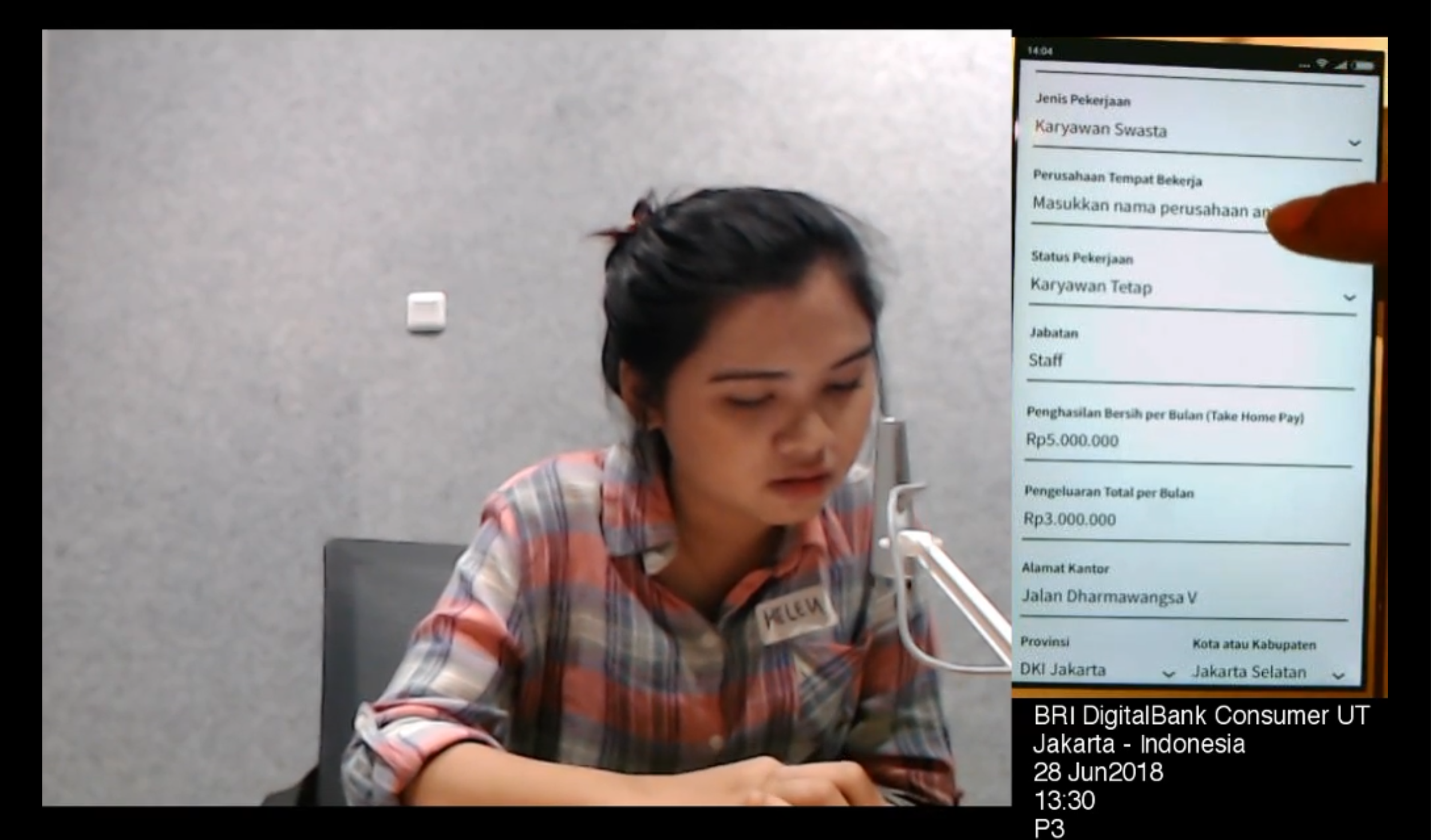

We made two versions of the digital prototype in low fidelity where the first prototype is to gain direct reference from competitors, while the second is a more refined version of the first prototype where all appropriate business requirements is implemented. We haven’t moved on to the final version because we still need to conduct Usability Testing to find out if all the design has answered the customer needs.

The wireframe focuses on onboarding and apply for limit credit primarily since it will determine if customers would be convinced enough to buy the product. For a faster and clear development process, we designed all screen steps in one single flow complete with interaction and detailed descriptions on what’s the content of the screen so that once everything is finalized after testing, the development team can locate and identify quickly for the user journey.

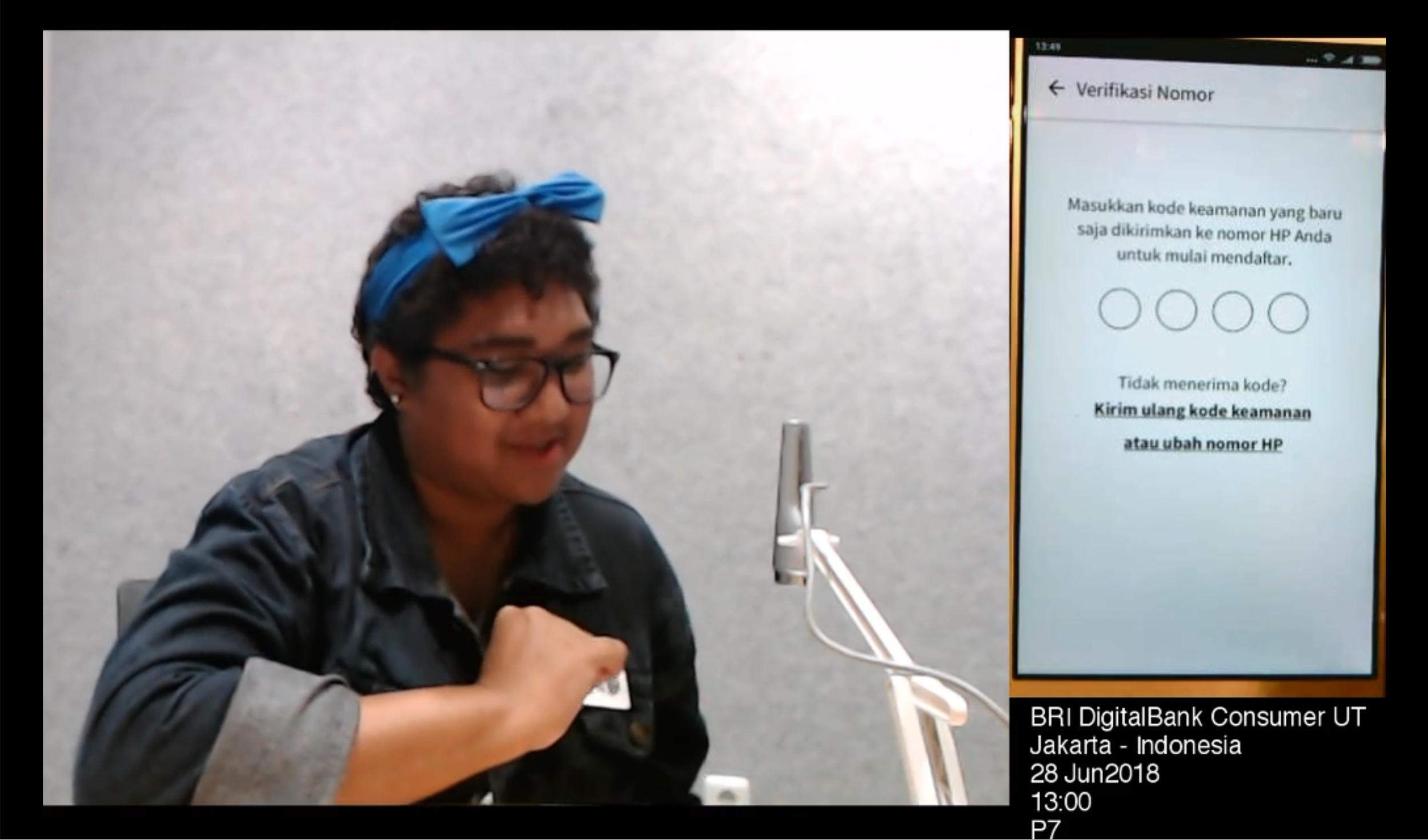

Usability Testing

When we conducted the low fidelity usability testing, we’ve learned that customers have positive impressions when they experience BRI’s first digital lending service. Majority of BRI customers have the perception that BRI is a micro service bank that was impossible to try pulling off an experience like this. Overall, it caught their attention when they see how the steps are simpler and easier to grasp, as well as the merchants that are available in the product gives more excitement for the customers.

Although there were some positive feedbacks, it comes with criticism that requires improvement on the design. The form design should be more short and customers expect to reduce the number of text fields being provided when they are applying for limit credit since the goal here is to obtain a huge number of customers. Customers also felt that waiting to verify email and the use of OTP is fairly new so they suggest that it should be placed easy enough for them to understand. Overall, when it comes to BRI customers, they are considered to be less tech-savy compare to other Banks in Indonesia. It is why the final design direction should try to cater these targeted audience.

Final Design

The Ceria application’s design focuses on readability and speed of experience. We used the decided color of purple to the final version to illustrate the smart and youthful brand for the apps. We wanted to make sure user goes through the details and read everything in detail so that they are able to accomplish applying for their limit credit. The journey is complementing both onboarding for education and development in order to have the apps running in the most sustainable way going forward.

In this final version of the app design, we focused primarily on the features of Onboarding, E-KYC, Online Transactions and Cash Out as the basic and fundamental of this application. What makes the experience of this design is unique for BRI is because it’s the first of its kind compare for a gov bank. Although other competitors may have done it before and launched it earlier, we managed to design it in such a way that it combines the company's compliance and the BRI customer needs therefore making it a sense of accomplishment.

Results & Key Learnings

Since its deployment, from what I can share is that we have obtained roughly about 60,000 new customers in the first month, adding 5% more new customers to the overall total of BRI’s customers. Although the number that gains is still small, BRI is able to obtain new customer profile that would help the business to target consumptive type customers in the future.

In this project, I would have to say my biggest learning is to never skip a UT in any possible way since it would help to avoid high risk when it is being developed. When we design, it has to come back to the user needs and wants. As a first official product design project, it feels overwhelming with the rigorous and detail process that I must pay attention. Also collaboration is key to make any product development a successful one.

In the next phase, what I would do differently is that I need to be better at collaborating with the development team in order to create the best experience in any way I can, as well as design with mind in priority and minimize freedom design unless given the chance. For the next stage as well in development, we would need to iterate on several features that require our attention internally and by looking at customers feedback